-

Audit of stand-alone annual accounts

At Grant Thornton Luxembourg, our team of experts is specialised in audits of stand-alone annual accounts.

-

Audit of consolidated annual accounts

Grant Thornton Luxembourg team of experts is specialised in providing audit services to a lot of multinational which have their administrative center located in Luxembourg for whom the consolidated annual accounts have to be audited.

-

Agreed-Upon Procedures Engagements

In the case of agreed-upon procedures engagement, Grant Thornton Luxembourg performs procedures particularly requested by the client/bank and reports on the findings.

-

GDPR-CARPA Certification

Grant Thornton Audit and Assurance is accredited by the Commission Nationale pour la Protection des Données (CNPD) to provide GDPR-CARPA certifications for organisations.

-

Forensic Audit

Grant Thornton Luxembourg has the forensic and business skills to deal with the most complex situations. A multi-disciplinary team of dedicated accountants in consultation with lawyers, IT consultants, insurance experts, valuation specialists and actuaries may be engaged when necessary.

-

Supervisory Auditor (Commissaire)

Grant Thornton Luxembourg has a dedicated team of experts committed to deliver services to reserved to Supervisory Auditor or "Commissaire aux Comptes".

-

Liquidation Audit

Grant Thornton Luxembourg has a dedicated team of experts committed to deliver services to reserved to liquidation audit "Commissariat à la liquidation".

-

Assurance Engagements

Grant Thornton Luxembourg have a dedicated team of experts committed to work on audit and assurance special engagements.

-

IFRS Services

At Grant Thornton Luxembourg, our experts can help you navigate the complexity of International Financial Reporting Standards (IFRS).

-

Valuation

Grant Thornton Luxembourg helps clients evaluate and implement various strategic alternatives through our comprehensive suite of corporate value consulting services. From opinions, board solutions and services, to valuation and modeling, we can assist you with value added services throughout the transaction lifecycle.

-

Business Risk Services

Mitigate risk and achieve compliance with solutions that address your unique challenges. From governance frameworks to risk assessments, we provide practical strategies to safeguard your business.

-

Consulting

Grant Thornton’s Consulting team is your trusted partner in transformation. We help you turn challenges into opportunities and lead your business confidently into the future.

-

Data Protection and Privacy

Protect your business and ensure regulatory compliance with tailored data privacy frameworks. We help you manage risks, meet GDPR requirements, and secure sensitive information.

-

Deal Advisory

Whether you’re navigating a merger, raising capital, or preparing for restructuring, Grant Thornton’s Deal Advisory team provides expert guidance to help you make informed decisions and achieve your goals.

-

Financial Accounting and Advisory Services (FAAS)

We bring practical solutions that facilitate your daily work, allowing you to focus on your business growth while ensuring compliance and efficiency in all financial matters. Let us guide you through the intricacies of financial accounting and advisory to set your business up for success.

-

Forensic Accounting

We provide customised forensic accounting solutions to help you uncover key facts, resolve disputes, and mitigate risks in multi-jurisdictional and complex environments.

-

Governance, Risk & Compliance

Navigate complex regulations and governance challenges with ease. We help you design and implement effective GRC frameworks that align with your strategic goals and meet regulatory requirements.

-

Sustainability & ESG Services

We empower organisations to define and achieve their environmental, social, and governance (ESG) goals with actionable strategies. Our comprehensive advisory services help you ensure compliance, improve performance, and build trust with stakeholders.

-

Whistleblowing Services

Create a culture of transparency and accountability. We assist in implementing robust whistleblowing frameworks, ensuring compliance with legal requirements and building trust within your organisation.

-

Alternative Investment Services

Grant Thornton Luxembourg is a bespoke business partner to established Alternative Investment Fund (“AIF”) Managers (“AIFM”) as well as independent Managers launching start-up Funds and seeking for a single entry point in Luxembourg in order to set-up and manage their Luxembourg domiciled Funds.

-

Fund Administration

Fund Administration - Grant Thornton Luxembourg offers a full range of tailored solutions to our clients.

-

Registrar & Transfer Agency Services, Client Reporting

Grant Thornton Luxembourg provides investors with confirmations, final Contract Notes and regular statements upon finalisation of the Fund’s Net Asset Value, We handle all wire payments and transfers, including the processing of distribution dividend payments, and perform in-depth Anti-Money Laundering Counter Terrorism Financing and Know-Your Client due diligence checks on investors.

-

Fund set-up, Launch & Corporate life

High-quality product structuring and legal services have become a crucial tool enabling industry players to get through the major changes impacting their business development, strategy and organisation as a whole. Our Investment Management practice at Grant Thornton Luxembourg is your one-stop place for expert advice combining pragmatism and a unique in-depth knowledge of the Luxembourg market.

-

AML Compliance Services

Grant Thornton Luxembourg helps its Clients to keep compliant with AML-CTF laws and regulations and provide an expert skilled team.

-

Regulatory Reporting Delivery

Grant Thornton Luxembourg has set up a Business Process Outsourcing Solution that manages and mutualises regulatory expertise, reporting solutions and skilled human resources

-

Legal Support & Corporate Services

Grant Thornton Luxembourg delivers Legal Support & Corporate services.

-

Accounting & Reporting Services

Grant Thornton Luxembourg may explore the specific characteristics of your company in order to provide a personalised assistance in the fields of Accounting & Reporting services.

-

Corporate Tax Compliance

Grant Thornton Luxembourg may explore the specific characteristics of your company in order to provide a personalised assistance in the fields of corporate tax compliance.

-

Corporate Finance

Exploring the strategic options available to you as a business or shareholder, advising and project managing the chosen solution, Grant Thornton Luxembourg provide a truly integrated corporate finance offering.

-

Corporate Secretarial Services

Grant Thornton Luxembourg provides corporate secretarial services to enable our clients to comply with their legal and administrative obligations in Luxembourg.

-

Cross-Border Tax

Tax policies are constantly evolving and there are a number of complex changes on the horizon that could significantly affect your business. We can help you with practical advice such as VAT and direct tax.

-

Direct Corporate Tax Advice

Grant Thornton Luxembourg understand the complexity of national and international tax laws. We can unlock your potential for local and international growth.

-

Expatriate Tax

Although international employment has become a standard practice in business life, employers and their assignees are still faced with numerous questions in this area. Grant Thornton Luxembourg can help you to be one step ahead.

-

HR Consulting

Entrust our experts with the outsourcing of your human resources to enable you to organise with complete serenity. You will save valuable time, boost your profitability and be able to concentrate on your core business!

-

Liquidation & Insolvency

Grant Thornton Luxembourg can draw on years of experience in the areas of liquidation and insolvency and then make sensible recommendations on how best to deal with your financial crisis.

-

Payroll

A team of highly qualified collaborators manages around 7,000 payslips per month and currently offers related consulting services to more than 500 clients. Our mission is to set up useful processes for the employer over the long term.

-

Personal Tax

Our experienced multilingual Personal Tax Team is keen to give you tailored solutions, optimise your situation and help you make decisions. We could assist you with: income tax returns, vat returns, tax assessments, contacts with the tax authorities and assistance by tax audit or tax litigation, tax matters advices, inheritance tax matters, international assignments and trainings.

-

Transaction & Reorganisation

Reorganisations - Transaction Planning - Tax Structuring - M&A. Companies strive to improve their market position with take-overs, mergers and demergers. Strategy and financial tactics are important elements in this respect. Grant Thornton tax specialists may intervene in all stages of the transaction.

-

Set-up, Restructuring & Business Planning

Grant Thornton Luxembourg is delighted to add value during the implementation of your businesses and to be given the opportunity to grow together with you. Relying on our professionals’ financial expertise will allow you to take dynamic but sustainable decisions.

-

Tax - Financial Services & Operational Tax

Our Tax - Financial Services team provides tax advisory services relevant for the Financial Services Industries and Operational Tax assistance. This includes tax advice, automatic exchange of information (FATCA, CRS, DAC 6, DAC 7 and DAC 8), advisory and compliance assistance regarding the US Qualified Intermediary (QI) regime, assistance regarding withholding tax reclaims, investor tax reporting and tax structuring in the context of Islamic finance.

-

Transfer Pricing

The laws surrounding transfer pricing are becoming ever more complex, as tax affairs of multinational companies are facing scrutiny from media, regulators and the public. Grant Thornton Luxembourg can help you manage your transfer pricing risks and find opportunities.

-

VAT and Other Indirect Tax Advice

Our VAT advisory business line is dedicated to keeping you up to date with amended VAT legislation and changes in the administrative practice in Luxembourg and worldwide with our Grant Thornton global VAT network. Specialists review and comment on new EU directives and the latest case law by the Court of Justice of the European Union in order to provide you with advice tailored to your specific needs.

-

VAT and Other Indirect Tax Compliance

Handling the day-to-day VAT compliance obligations requires being close to your business. Our VAT compliance business line assists you to ensure that long term reporting processes are implemented and respected with the aim of safeguarding a proper and timely VAT filing. This is important for achieving a VAT compliant environment and mitigating local VAT risks.

-

Information Security

Is your organisation resilient to information security threats? Whether you're a large enterprise or a small business, Grant Thornton is committed to providing comprehensive security services tailored to your needs.

-

IT Audit

Grant Thornton internal audit team provides IT audit services as part of your internal audit or as part of any specific IT audit that is required (ad’hoc , assurance reports, external audits).

-

MySmartOffice

Grant Thornton Luxembourg offers a new complete online accounting and consulting solution for SMEs named MySmartOffice to access financial and operational information instantly online.

Background

BEFIT was first announced in May 2021 in the EC’s Communication on Business Taxation for the 21st Century. The EC considers that common rules to calculate the taxable income of businesses operating in the EU are needed because it is difficult and costly for businesses to comply with (up to) 27 different national tax systems. The Proposal aims to create a level playing field, enhance legal certainty, reduce compliance costs, encourage businesses to operate cross-border, and stimulate investments and growth in the EU.

1. Entities in scope

The BEFIT proposal provides for a hybrid scope for the application of the rules, namely a mandatory and a voluntary one. The former covers:

- Domestic and MNEs operating in the EU, either headquartered in the EU or in a third country with an annual global turnover of at least EUR 750 million in at least two of the last four fiscal years; and

- Where the ultimate parent entity (“UPE”) holds, directly or indirectly, at least 75% of the ownership rights or of the rights giving entitlement to profit.

However, for groups headquartered in third countries, the rules of the Proposal will not apply if in two of the last four years, the combined revenues of the group’s EU subsidiaries and permanent establishments (“PEs”) do not exceed (i) 5% of the total group revenues or (ii) EUR 50 million.

There is also a voluntary application of the rules for entities which prepare consolidated financial statements and for which the abovementioned scoping thresholds are not met.

2. Common rules to calculate the tax base

To calculate the BEFIT tax base, each member of the BEFIT group will compute its preliminary tax result by adjusting its financial accounting net income or loss for the financial year as determined by a single accounting standard. In particular, this is the standard used in the preparation of the consolidated financial statements of the UPE.

This mechanism could resemble the Global Anti-Base Erosion Model Rules (“Pillar Two”), however, it involves fewer adjustments. Consequently, achieving compliance should, in theory, pose fewer challenges for MNEs within its scope. However, it is worth noting that potential duplications in calculations could arise if companies are required to independently ensure compliance with both regulatory frameworks.

3. Aggregation of the tax base at EU group level

Following the calculation of the preliminary tax result, the tax bases are aggregated to the BEFIT tax base. In case the BEFIT tax base is positive, the profit is allocated among the entities. In the case the tax base is negative, the loss is carried forward and shall be set off against the next positive BEFIT tax base.

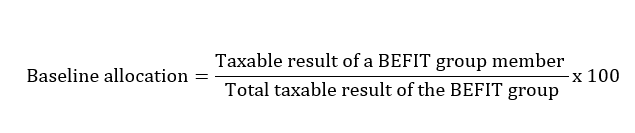

4. Allocation of the aggregated tax base

The BEFIT taxable base is allocated to the BEFIT group members under a baseline allocation percentage and is determined as follows:

Where:

- the taxable result of a BEFIT group member: the average of the taxable results in the three previous fiscal years

- taxable result of the BEFIT group: the addition of the average of the taxable results, as referred to in point (i), of all BEFIT group members in the three previous fiscal years.

Additionally, in case a BEFIT group member has a negative taxable result, it shall have its baseline allocation percentage set at zero.

5. Member States’ taxation autonomy

Based on the Proposal, Member States retain the flexibility to adjust their portion of the tax base using national regulations. This flexibility allows Member States to tailor their tax systems to align with their unique tax policy objectives.

This could encompass local tax incentives or deductions, provided they remain consistent with the Pillar Two requirements. It is important to note that Member States retain control over tax rates and enforcement policies.

6. Simplified TP approach

The Proposal introduces a simplified TP approach for assessing intercompany transactions involving low-risk distribution and manufacturing activities between a member of the BEFIT group and associated enterprises outside the BEFIT group. In this approach, taxpayers will have their results compared with a regional benchmark analysis prepared by the EC.

Based on this comparison, taxpayers will be classified as low, medium, or high risk, which will have an impact on the probability of tax audits or inquiries by tax authorities.

7. Our observations

If adopted, Member States should implement BEFIT by 1 January 2028 and apply its provisions from 1 July 2028. We anticipate that BEFIT might have a major impact on the tax calculation and administration of MNEs with a European footprint.

While it is not yet possible to anticipate whether the Proposal will eventually be adopted (unanimous approval by EU Member States is required), we would recommend to businesses in scope to carefully monitor the development of the Proposal.

Should you have any questions on that matter, please do not hesitate to reach out to the Tax team at Grant Thornton Luxembourg.

- Jean-Nicolas Bourtembourg - Partner, Head of Tax & Transfer Pricing

- Mélina Rondeux - Partner, Tax Compliance