We remind you of the importance of analysing your situation:

Are you affected by the QM ruling?

Are you compliant from a salary and accounting perspective?

Company cars: Update

-

Benefit in kind

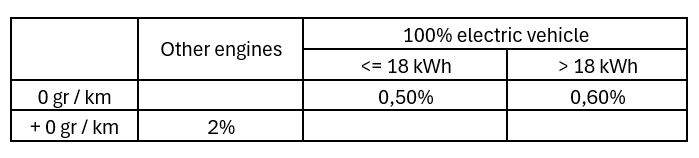

As of January 1st, 2025, the applicable rates for calculating your employees’ car benefit in kind are as follow:

This only applies to vehicles registered on or after January 1st, 2025, which have not been covered by a contract signed before January 1st, 2025.

-

VAT

-

-

Principles

-

On January 20th, 2021, the Court of Justice of the European Union issued a ruling (the « QM » judgment) providing guidance on the circumstances in which the provision of a vehicle may be classified as a « long-term hiring of means of transport » and the resulting implications.

Three cumulative conditions must be met in order to qualify as a long-term hiring of means of transport:

- The vehicle must be made available to the employee for a period of more than 30 consecutive days;

- The employee must have the permanent right to use the vehicle for private purposes;

- A compensation must be paid. The vehicle must be provided « for consideration » by either:

-

- Payment by the employee to the employer;

- The employer withholding part of the employee’s remuneration;

- The employee choosing between different benefits offered by the employer, based on an agreement between the parties whereby the right to use the company car implies the renunciation of other benefits.

As a result, companies operating this way will be subject to these new rules, which now provide that company cars will be subject to VAT in the employee’s country of residence.

NEWS: The French tax authorities have issued the following clarifications:

- Taxation takes place in the employee’s country of residence when the provision is made with consideration.

- Taxation takes place in the employer’s country of residence when the provision is made without consideration.

-

-

Impacts

-

This decision will result in VAT obligations for the employer in the employee's country of residence:

- Both residents and non-resident employees will be liable for VAT, which will affect their salary calculation.

- The employer will have to collect, declare, and pay this VAT to the authorities in the employee’s country of residence. This can be done through the single European registration system « MOSS », or through direct registration in the employee’s country of residence.

In order to comply with this circular, the companies concerned must estimate for each of their employee the share of VAT due to the country of residence, according to the calculation methods specific to each country, and deduct this amount via the salary.

Contact

Any questions? Don't hesitate to contact our experts: HumanCapitalServices@lu.gt.com.