Background and summary

The reverse hybrid entity rules were introduced into the domestic law following the implementation of the Anti-Tax Avoidance Directive 2 (“ATAD 2”) and are applicable as from tax year 2022.

The reverse hybrid entity rules apply to Luxembourg tax transparent entities (e.g., SCS or SCSp), provided that certain conditions are met. The Luxembourg partnership has to be owned by one or more non-resident associated enterprises (individuals or entities) which:

- consider the Luxembourg partnership as opaque; and

- hold directly or indirectly a participation of at least 50% in terms of voting rights or capital ownership (or are entitled to receive at least 50% of the profit) in the Luxembourg partnership (i.e. the related party test).

Based on the reverse hybrid rules, a reverse hybrid entity may become subject to corporate income tax (“CIT”) on the portion of its net taxable income which is not otherwise taxed in Luxembourg or any other jurisdiction.

The Circular clarifies the tax status of a reverse hybrid entity and provides guidance on the determination of its total net income. Its tax compliance obligations are further explained in the FAQ.

The Circular reminds also the the reverse hybrid rules are not applicable to some Collective Investment Funds.

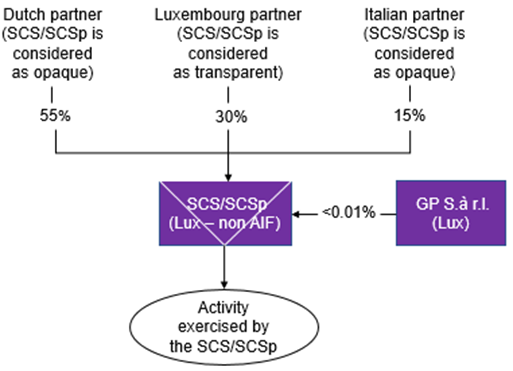

1. Example of an SCS/SCSp reverse hybrid entity

In this example, the impact will be the following as from tax year 2022:

- 55% of the profits of the SCS/SCSp are subject to CIT (i.e., profits attributable to the Dutch partner);

- 15% attributable to the Italian partner is not subject to CIT as long as it can be demonstrated that he is not acting together with the Dutch partner.

2. The Circular

Tax status of a reverse hybrid entity

Based on the Circular, reverse hybrid entities should not be considered as resident corporate entities within the meaning of article 159 of the LITL. Therefore, certain provisions applying to corporate entities are not applicable to reverse hybrid entities. Namely, the Circular specifies that articles 164ter (controlled foreign companies), 166 (participation exemption), 168bis (interest deduction limitation rules) and 168ter (anti-hybrid rules) L.I.R. are not applicable.

Determination of the total net income subject to tax

Firstly, the Circular notes that the net income of a reverse hybrid entity which may be subject to CIT includes the following types of income:

- net income from movable capital (article 97 LITL);

- net rental income (article 98 LITL);

- other net income (article 99 LITL).

Taxable basis is to be determined based on the above income realised by the reverse hybrid entity during the calendar year (1 January – 31 December), regardless of whether the reverse hybrid has an accounting year differing from the calendar year.

In case where income and expenses of a reverse hybrid entity are denominated in a foreign currency, the conversion of the amounts should be made, in principle, at the exchange rate on the day of the receipt of the income or the incurrence of the expense. However, the Circular allows, by way of administrative tolerance, conversion into EUR either at the year-end exchange rate or at the average exchange rate for the tax year in question.

Furthermore, the Circular specifies that falling within the scope of a reverse hybrid entity does not lead to application of a step up in value. Therefore, no capital gain should be realised upon this event. Ceasing to be considered a reverse hybrid entity has no Luxembourg tax consequences either.

The Circular further confirms that income distributions from a reverse hybrid entity to its partners are not subject to withholding tax (“WHT”).

Even if the participation exemption may not apply at the level of a reverse hybrid entity, dividends received by such entity may still benefit from a 50% exemption (article 115 (15a) LITL), provided that the applicable conditions are met.

Finally, the Circular notes that when the total net income of a reverse hybrid entity contains net income from movable capital (article 97 LITL) subject to WHT at source, tax withheld will be creditable proportionally to the part of the income subject to CIT at the level of the reverse hybrid entity.

3. Form 205

A new tax form 205 has been issued by the Luxembourg tax authorities. The filing obligation lies with all transparent entities that have received a request to file by the LTA, as well as transparent entities qualifying as reverse hybrid entities by application of article 168quater.

The form itself consists of two parts – the determination of the total net income of the entity and the net income subject to corporate income tax in Luxembourg.

The FAQ related to the form 205 clarifies that its filing is mutually exclusive with filing the forms 200 and 300.

4. Our observations

We would recommend Luxembourg transparent entities (such as SCS or SCSp) to firstly consider the potential application of article 168quater and, if applicable, clarifications provided by the LTA in the Circular and the FAQ.

The deadline to file the tax form 205 for tax year 2022 is 31 December 2023.

Should you be in need of assistance regarding the reverse hybrid rules and their impact on your business or tax compliance obligations of the reverse hybrid entities, please contact the Tax team at Grant Thornton Luxembourg.

- Jean-Nicolas Bourtembourg - Partner, Head of Tax & Transfer Pricing

- Mélina Rondeux - Partner, Tax Compliance