-

Audit of stand-alone annual accounts

At Grant Thornton Luxembourg, our team of experts is specialised in audits of stand-alone annual accounts.

-

Audit of consolidated annual accounts

Grant Thornton Luxembourg team of experts is specialised in providing audit services to a lot of multinational which have their administrative center located in Luxembourg for whom the consolidated annual accounts have to be audited.

-

Agreed-Upon Procedures Engagements

In the case of agreed-upon procedures engagement, Grant Thornton Luxembourg performs procedures particularly requested by the client/bank and reports on the findings.

-

GDPR-CARPA Certification

Grant Thornton Audit and Assurance is accredited by the Commission Nationale pour la Protection des Données (CNPD) to provide GDPR-CARPA certifications for organisations.

-

Forensic Audit

Grant Thornton Luxembourg has the forensic and business skills to deal with the most complex situations. A multi-disciplinary team of dedicated accountants in consultation with lawyers, IT consultants, insurance experts, valuation specialists and actuaries may be engaged when necessary.

-

Supervisory Auditor (Commissaire)

Grant Thornton Luxembourg has a dedicated team of experts committed to deliver services to reserved to Supervisory Auditor or "Commissaire aux Comptes".

-

Liquidation Audit

Grant Thornton Luxembourg has a dedicated team of experts committed to deliver services to reserved to liquidation audit "Commissariat à la liquidation".

-

Assurance Engagements

Grant Thornton Luxembourg have a dedicated team of experts committed to work on audit and assurance special engagements.

-

IFRS Services

At Grant Thornton Luxembourg, our experts can help you navigate the complexity of International Financial Reporting Standards (IFRS).

-

Valuation

Grant Thornton Luxembourg helps clients evaluate and implement various strategic alternatives through our comprehensive suite of corporate value consulting services. From opinions, board solutions and services, to valuation and modeling, we can assist you with value added services throughout the transaction lifecycle.

-

Business Risk Services

Mitigate risk and achieve compliance with solutions that address your unique challenges. From governance frameworks to risk assessments, we provide practical strategies to safeguard your business.

-

Consulting

Grant Thornton’s Consulting team is your trusted partner in transformation. We help you turn challenges into opportunities and lead your business confidently into the future.

-

Data Protection and Privacy

Protect your business and ensure regulatory compliance with tailored data privacy frameworks. We help you manage risks, meet GDPR requirements, and secure sensitive information.

-

Deal Advisory

Whether you’re navigating a merger, raising capital, or preparing for restructuring, Grant Thornton’s Deal Advisory team provides expert guidance to help you make informed decisions and achieve your goals.

-

Financial Accounting and Advisory Services (FAAS)

We bring practical solutions that facilitate your daily work, allowing you to focus on your business growth while ensuring compliance and efficiency in all financial matters. Let us guide you through the intricacies of financial accounting and advisory to set your business up for success.

-

Forensic Accounting

We provide customised forensic accounting solutions to help you uncover key facts, resolve disputes, and mitigate risks in multi-jurisdictional and complex environments.

-

Governance, Risk & Compliance

Navigate complex regulations and governance challenges with ease. We help you design and implement effective GRC frameworks that align with your strategic goals and meet regulatory requirements.

-

Sustainability & ESG Services

We empower organisations to define and achieve their environmental, social, and governance (ESG) goals with actionable strategies. Our comprehensive advisory services help you ensure compliance, improve performance, and build trust with stakeholders.

-

Whistleblowing Services

Create a culture of transparency and accountability. We assist in implementing robust whistleblowing frameworks, ensuring compliance with legal requirements and building trust within your organisation.

-

Alternative Investment Services

Grant Thornton Luxembourg is a bespoke business partner to established Alternative Investment Fund (“AIF”) Managers (“AIFM”) as well as independent Managers launching start-up Funds and seeking for a single entry point in Luxembourg in order to set-up and manage their Luxembourg domiciled Funds.

-

Fund Administration

Fund Administration - Grant Thornton Luxembourg offers a full range of tailored solutions to our clients.

-

Registrar & Transfer Agency Services, Client Reporting

Grant Thornton Luxembourg provides investors with confirmations, final Contract Notes and regular statements upon finalisation of the Fund’s Net Asset Value, We handle all wire payments and transfers, including the processing of distribution dividend payments, and perform in-depth Anti-Money Laundering Counter Terrorism Financing and Know-Your Client due diligence checks on investors.

-

Fund set-up, Launch & Corporate life

High-quality product structuring and legal services have become a crucial tool enabling industry players to get through the major changes impacting their business development, strategy and organisation as a whole. Our Investment Management practice at Grant Thornton Luxembourg is your one-stop place for expert advice combining pragmatism and a unique in-depth knowledge of the Luxembourg market.

-

AML Compliance Services

Grant Thornton Luxembourg helps its Clients to keep compliant with AML-CTF laws and regulations and provide an expert skilled team.

-

Regulatory Reporting Delivery

Grant Thornton Luxembourg has set up a Business Process Outsourcing Solution that manages and mutualises regulatory expertise, reporting solutions and skilled human resources

-

Legal Support & Corporate Services

Grant Thornton Luxembourg delivers Legal Support & Corporate services.

-

Accounting & Reporting Services

Grant Thornton Luxembourg may explore the specific characteristics of your company in order to provide a personalised assistance in the fields of Accounting & Reporting services.

-

Corporate Tax Compliance

Grant Thornton Luxembourg may explore the specific characteristics of your company in order to provide a personalised assistance in the fields of corporate tax compliance.

-

Corporate Finance

Exploring the strategic options available to you as a business or shareholder, advising and project managing the chosen solution, Grant Thornton Luxembourg provide a truly integrated corporate finance offering.

-

Corporate Secretarial Services

Grant Thornton Luxembourg provides corporate secretarial services to enable our clients to comply with their legal and administrative obligations in Luxembourg.

-

Cross-Border Tax

Tax policies are constantly evolving and there are a number of complex changes on the horizon that could significantly affect your business. We can help you with practical advice such as VAT and direct tax.

-

Direct Corporate Tax Advice

Grant Thornton Luxembourg understand the complexity of national and international tax laws. We can unlock your potential for local and international growth.

-

Expatriate Tax

Although international employment has become a standard practice in business life, employers and their assignees are still faced with numerous questions in this area. Grant Thornton Luxembourg can help you to be one step ahead.

-

HR Consulting

Entrust our experts with the outsourcing of your human resources to enable you to organise with complete serenity. You will save valuable time, boost your profitability and be able to concentrate on your core business!

-

Liquidation & Insolvency

Grant Thornton Luxembourg can draw on years of experience in the areas of liquidation and insolvency and then make sensible recommendations on how best to deal with your financial crisis.

-

Payroll

A team of highly qualified collaborators manages around 7,000 payslips per month and currently offers related consulting services to more than 500 clients. Our mission is to set up useful processes for the employer over the long term.

-

Personal Tax

Our experienced multilingual Personal Tax Team is keen to give you tailored solutions, optimise your situation and help you make decisions. We could assist you with: income tax returns, vat returns, tax assessments, contacts with the tax authorities and assistance by tax audit or tax litigation, tax matters advices, inheritance tax matters, international assignments and trainings.

-

Transaction & Reorganisation

Reorganisations - Transaction Planning - Tax Structuring - M&A. Companies strive to improve their market position with take-overs, mergers and demergers. Strategy and financial tactics are important elements in this respect. Grant Thornton tax specialists may intervene in all stages of the transaction.

-

Set-up, Restructuring & Business Planning

Grant Thornton Luxembourg is delighted to add value during the implementation of your businesses and to be given the opportunity to grow together with you. Relying on our professionals’ financial expertise will allow you to take dynamic but sustainable decisions.

-

Tax - Financial Services & Operational Tax

Our Tax - Financial Services team provides tax advisory services relevant for the Financial Services Industries and Operational Tax assistance. This includes tax advice, automatic exchange of information (FATCA, CRS, DAC 6, DAC 7 and DAC 8), advisory and compliance assistance regarding the US Qualified Intermediary (QI) regime, assistance regarding withholding tax reclaims, investor tax reporting and tax structuring in the context of Islamic finance.

-

Transfer Pricing

The laws surrounding transfer pricing are becoming ever more complex, as tax affairs of multinational companies are facing scrutiny from media, regulators and the public. Grant Thornton Luxembourg can help you manage your transfer pricing risks and find opportunities.

-

VAT and Other Indirect Tax Advice

Our VAT advisory business line is dedicated to keeping you up to date with amended VAT legislation and changes in the administrative practice in Luxembourg and worldwide with our Grant Thornton global VAT network. Specialists review and comment on new EU directives and the latest case law by the Court of Justice of the European Union in order to provide you with advice tailored to your specific needs.

-

VAT and Other Indirect Tax Compliance

Handling the day-to-day VAT compliance obligations requires being close to your business. Our VAT compliance business line assists you to ensure that long term reporting processes are implemented and respected with the aim of safeguarding a proper and timely VAT filing. This is important for achieving a VAT compliant environment and mitigating local VAT risks.

-

Information Security

Is your organisation resilient to information security threats? Whether you're a large enterprise or a small business, Grant Thornton is committed to providing comprehensive security services tailored to your needs.

-

IT Audit

Grant Thornton internal audit team provides IT audit services as part of your internal audit or as part of any specific IT audit that is required (ad’hoc , assurance reports, external audits).

-

MySmartOffice

Grant Thornton Luxembourg offers a new complete online accounting and consulting solution for SMEs named MySmartOffice to access financial and operational information instantly online.

Background and summary

The reverse hybrid entity rules were introduced into the domestic law following the implementation of the Anti-Tax Avoidance Directive 2 (“ATAD 2”) and are applicable as from tax year 2022.

The reverse hybrid entity rules apply to Luxembourg tax transparent entities (e.g., SCS or SCSp), provided that certain conditions are met. The Luxembourg partnership has to be owned by one or more non-resident associated enterprises (individuals or entities) which:

- consider the Luxembourg partnership as opaque; and

- hold directly or indirectly a participation of at least 50% in terms of voting rights or capital ownership (or are entitled to receive at least 50% of the profit) in the Luxembourg partnership (i.e. the related party test).

Based on the reverse hybrid rules, a reverse hybrid entity may become subject to corporate income tax (“CIT”) on the portion of its net taxable income which is not otherwise taxed in Luxembourg or any other jurisdiction.

The Circular clarifies the tax status of a reverse hybrid entity and provides guidance on the determination of its total net income. Its tax compliance obligations are further explained in the FAQ.

The Circular reminds also the the reverse hybrid rules are not applicable to some Collective Investment Funds.

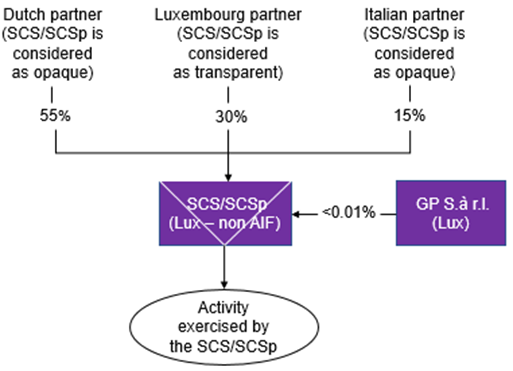

1. Example of an SCS/SCSp reverse hybrid entity

In this example, the impact will be the following as from tax year 2022:

- 55% of the profits of the SCS/SCSp are subject to CIT (i.e., profits attributable to the Dutch partner);

- 15% attributable to the Italian partner is not subject to CIT as long as it can be demonstrated that he is not acting together with the Dutch partner.

2. The Circular

Tax status of a reverse hybrid entity

Based on the Circular, reverse hybrid entities should not be considered as resident corporate entities within the meaning of article 159 of the LITL. Therefore, certain provisions applying to corporate entities are not applicable to reverse hybrid entities. Namely, the Circular specifies that articles 164ter (controlled foreign companies), 166 (participation exemption), 168bis (interest deduction limitation rules) and 168ter (anti-hybrid rules) L.I.R. are not applicable.

Determination of the total net income subject to tax

Firstly, the Circular notes that the net income of a reverse hybrid entity which may be subject to CIT includes the following types of income:

- net income from movable capital (article 97 LITL);

- net rental income (article 98 LITL);

- other net income (article 99 LITL).

Taxable basis is to be determined based on the above income realised by the reverse hybrid entity during the calendar year (1 January – 31 December), regardless of whether the reverse hybrid has an accounting year differing from the calendar year.

In case where income and expenses of a reverse hybrid entity are denominated in a foreign currency, the conversion of the amounts should be made, in principle, at the exchange rate on the day of the receipt of the income or the incurrence of the expense. However, the Circular allows, by way of administrative tolerance, conversion into EUR either at the year-end exchange rate or at the average exchange rate for the tax year in question.

Furthermore, the Circular specifies that falling within the scope of a reverse hybrid entity does not lead to application of a step up in value. Therefore, no capital gain should be realised upon this event. Ceasing to be considered a reverse hybrid entity has no Luxembourg tax consequences either.

The Circular further confirms that income distributions from a reverse hybrid entity to its partners are not subject to withholding tax (“WHT”).

Even if the participation exemption may not apply at the level of a reverse hybrid entity, dividends received by such entity may still benefit from a 50% exemption (article 115 (15a) LITL), provided that the applicable conditions are met.

Finally, the Circular notes that when the total net income of a reverse hybrid entity contains net income from movable capital (article 97 LITL) subject to WHT at source, tax withheld will be creditable proportionally to the part of the income subject to CIT at the level of the reverse hybrid entity.

3. Form 205

A new tax form 205 has been issued by the Luxembourg tax authorities. The filing obligation lies with all transparent entities that have received a request to file by the LTA, as well as transparent entities qualifying as reverse hybrid entities by application of article 168quater.

The form itself consists of two parts – the determination of the total net income of the entity and the net income subject to corporate income tax in Luxembourg.

The FAQ related to the form 205 clarifies that its filing is mutually exclusive with filing the forms 200 and 300.

4. Our observations

We would recommend Luxembourg transparent entities (such as SCS or SCSp) to firstly consider the potential application of article 168quater and, if applicable, clarifications provided by the LTA in the Circular and the FAQ.

The deadline to file the tax form 205 for tax year 2022 is 31 December 2023.

Should you be in need of assistance regarding the reverse hybrid rules and their impact on your business or tax compliance obligations of the reverse hybrid entities, please contact the Tax team at Grant Thornton Luxembourg.

- Jean-Nicolas Bourtembourg - Partner, Head of Tax & Transfer Pricing

- Mélina Rondeux - Partner, Tax Compliance