Receive the latest insights, news and more direct to your inbox.

Contents

Subscribe to our mailing list

Since the introduction of the European Central Bank (ECB) supervisory expectations for Climate-related & Environmental Risks, now Climate and Nature (C&N), formalised in the ECB Guide of November 2020[1] and the 2025 press release[2], the materiality assessment has served as a foundational requirement for integrating C&N risks into institutions’ enterprise-wide risk management frameworks. Over the past years, this early regulatory push ensured that the methodology for assessing climate risk materiality became both familiar and widely embedded across institutions.

With the publication of the European Banking Authority (EBA) Guidelines on the management of Environmental, Social and Governance (ESG) risks on 9 January 2025[3], credit institutions are now required to broaden their risk lens. The scope has expanded beyond C&N risks to also encompass Social and Governance risks.

This evolving regulatory environment now pushes institutions to ask themselves: Can existing C&N risk materiality assessments be extended to capture social risks, or is a more tailored approach needed?

The ESG Risk Materiality Requirements

Under the EBA Guidelines, institutions must carry out regular ESG materiality assessments: annually for most institutions and every two years for smaller, non-complex institutions (SNCI). This requirement reinforces that credit institutions must rigorously assess ESG risks, rather than only focusing on the C&N drivers. As a result, institutions must reconsider whether the “more traditional” C&N materiality assessment can adequately capture these risks, or whether more structured adaptations are needed.

Generally, for most institutions, governance risks tend to be well‑structured, audited, and embedded across compliance, internal audit, business activities and risk functions. Social‑related considerations are often addressed across various departments, including human resources, conduct, product oversight, customer protection, corporate responsibility, though typically without a single overarching framework linking these activities together.

Social risks, such as customer vulnerability and fair treatment matters, are inherently cross‑cutting and differ from C&N risks, as they are shaped by distinct risk drivers (including C&N drivers), rely on broader and more diverse data sources, and affect a wide range of stakeholders across multiple areas of an institution’s operations. They also unfold over different time horizons and through complex, multifaceted impact pathways. Because of this wide reach and unique structure, simply extending an existing C&N risk materiality approach without adapting it to these characteristics would not provide a complete and reliable assessment of social risks.

Our Approach to Social Risk Materiality Assessment

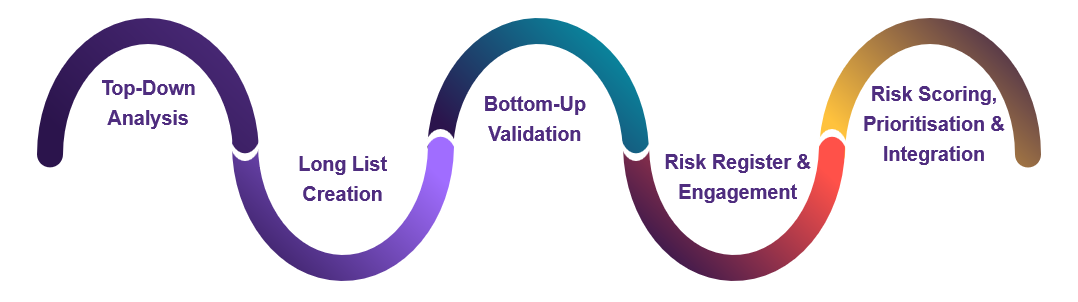

At Grant Thornton, we recognise the market’s challenge in operationalising social risk within existing structures. To support institutions, we developed a Social Risk Materiality Assessment that:

- follows the familiar structure and principles of C&N risk materiality assessments

- expands the scope to capture the full range of social risk drivers

- centralises social considerations that were previously scattered across departments

Our framework helps institutions understand how a range of social factors, such as customer vulnerability, financial inclusion, employee well-being, conduct, community impact, and societal expectations, and others, may affect: Operational Resilience, Reputation, Customer Trust, Strategic Outcomes, and Long-term Sustainability.

Our approach helps financial institutions identify and prioritise social risks through a structured assessment that combines regulatory insight[4], business context, and internal validation. The process is designed to support clearer identification of social risk themes and stronger integration into existing risk management structures.

Conclusion

Social risk has always been inherent to financial institutions and the communities they serve, but its significance is becoming increasingly pronounced as societal expectations, regulatory standards, and global trends continue to evolve. In this context, having a clear, documented, and repeatable methodology for assessing social risks over time is essential, not only to understand today’s exposures, but to anticipate how these risks will shift alongside demographic changes, societal pressures, and broader transformations such as the transition to net zero and the impacts of climate warming. Establishing a structured approach enables institutions to engage proactively, respond consistently, and strengthen the resilience and accountability of their risk management frameworks as social risks continue to develop in complexity and scope.

Contact

If you wish to understand how you could best implement the EBA Guidelines on the management of ESG risks, conduct a Social Risk Materiality Assessment and integrate ESG risks in the enterprise risk management framework, please contact Janice Daly, Advisory Partner at Grant Thornton Ireland or Dara Kelly, Head of Advisory at Grant Thornton Luxembourg.

[1] ECB Guide on climate-related and environmental risks

[4] This includes the EBA Guidelines, the Commission de Surveillance du Secteur Financier (CSSF)’s supervisory priorities in the area of sustainable finance, the European Sustainability Reporting Standards (ESRS), the Principles for Responsible Banking (PRB), the Taskforce on Inequality and Social‑related Financial Disclosures (TISFD), and the Organisation for Economic Co-operation and Development (OECD) Guidelines for Multinational Enterprises on Responsible Business Conduct.